Private wealth vs. Personal strategy: which one gives you more confidence in a complex year

A big income jump, a large stock sale, or a net worth that puts you in a new bracket are milestone financial events. You know you’re ready for a more thoughtful approach to wealth management, but you’re not sure what’s best for your situation: building a personal strategy focused on your specific goals or the broad infrastructure of an established firm.

Let’s break down the difference between these two structures.

In this article

- Divorce decisions aren’t just financial. They’re a mix of math, emotion, and long-term life design, and all three matter.

- The goal isn’t to “win” every category, but to make smart tradeoffs that protect both your financial future and your emotional bandwidth.

- The best settlements often come from honoring both stability and flexibility, so you can move forward without resentment or regret.

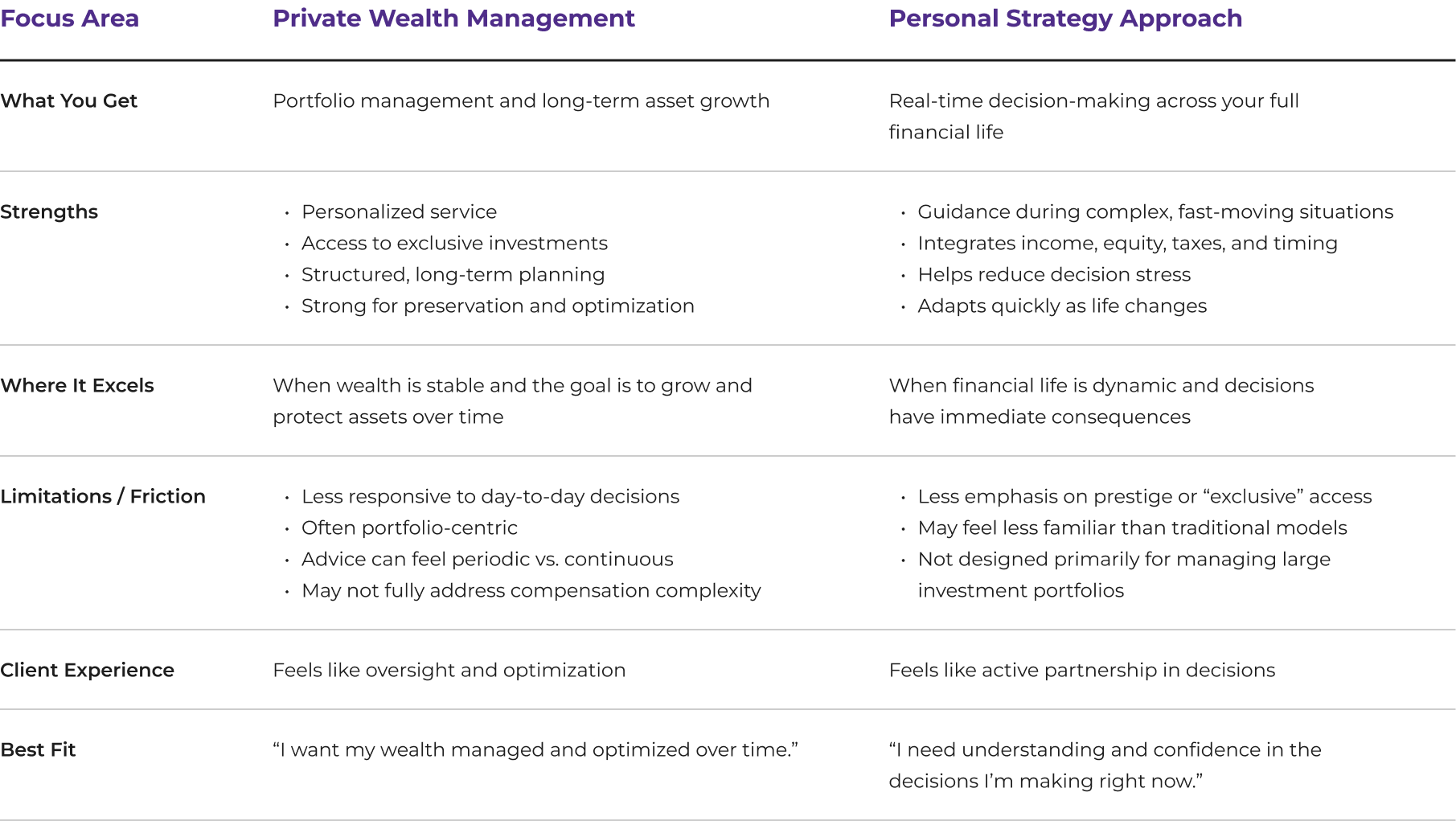

Traditional wealth firms focus on keeping large assets safe

Traditional private wealth management is what happens when you hand your money over to a giant financial institution like J.P. Morgan, Goldman Sachs, or Morgan Stanley. These firms are built to do one thing well: protect massive amounts of wealth. You’re paying for the reputation, the giant legal teams, and the stability that comes with a global brand. If you need a multi-million-dollar loan for commercial real estate or you’re managing assets across multiple countries, these institutions have the infrastructure to handle it.

When a company manages billions of dollars for thousands of people, however, you are not getting a deeply personalized experience. You’re getting a system with the same rules, the same process, and the same categories based mostly on how much money you have. To be fair, that model works for some people. These Wall Street titans wouldn’t be in business if their money management approaches weren’t successful.

But their job is to preserve wealth, not necessarily help you navigate messy financial decisions in your life like trying to sell a business or getting help with complicated stock options. Maybe most of your financial stress has nothing to do with your investment portfolio and everything to do with taxes, ownership, or cash flow.

That’s where the big-bank model can start to feel frustrating. Because their systems are designed for consistency, not flexibility, they often try to fit people into prebuilt packages instead of solving the actual problem in front of them. And since they make money managing your investments, that’s usually where the focus stays.

A personal strategy makes all your moving pieces work together

A personalized financial strategy does the opposite of the traditional big-bank model. Instead of placing you into a prebuilt tier based on your net worth, it builds a plan around your compensation, your taxes, your business decisions, and your cash flow.

For most people with complex finances, the biggest problem is not a lack of investment options. It’s that none of their advisors are talking to each other. Your CPA is focused on taxes. Your estate attorney is focused on legal protection. Your investment advisor is focused on your portfolio. Meanwhile, you’re stuck trying to connect all the dots yourself. A strategy-first approach focuses on getting all the pieces working together.

Let’s say you’re dealing with stock options, deferred compensation, concentrated stock positions, or a business sale. You need advice that looks at the full picture, not just someone trying to sell you a financial product. But be prepared. This kind of relationship is more hands-on. You’ll have to engage with your financial decisions instead of handing everything over to someone.

So if your goal is simple, like buying index funds, automating your investing, and moving on with your life, you probably do not need this level of strategy. But if your financial life has moving parts, big decisions, or tax complexity, having someone coordinate the entire picture can save you a massive amount of money and stress over time.

The emotional experience of each model can feel different

With traditional private wealth management, the emotional win is in the delegation. You feel supported because an established system is absorbing all the complexity for you. There is a sense of comfort in their hierarchy, strict processes, and infrastructure. That experience can feel incredibly grounding during periods of market uncertainty.

In a personal strategy model, the emotional win comes from visibility and active participation. You feel deeply connected to your financial decisions because the plan is built around your goals. You aren't just handing over the keys; you are sitting in the co-pilot seat.

Neither experience is better than the other. Some people want a firm handling every moving part behind the scenes so they never have to think about it. Others want collaborative conversations that evolve alongside their career, family priorities, and changing lives.

Financial complexity changes the kind of financial support you need

If you’re overwhelmed tracking vesting schedules, tax exposure, and estate maintenance on your own, the advisors at CURO can help. Let us take the administrative weight off your shoulders so managing your wealth stops feeling like a second job.

CURO Wealth Management does not provide legal or tax advice. You should consult a legal or tax professional regarding your individual situation.