Math vs. Emotion: 5 divorce decisions that honor both—and why it’s important to do so

Most divorce financial advice encourages setting emotions aside. It can sound like friends saying, “Think with your head, not with your heart.” Or maybe it’s your family saying, “Take the deal that looks best on paper.”

But divorce isn’t just a simple math problem to solve. Stability, autonomy, time with your kids, emotional bandwidth, freedom to move. These things don’t fit neatly into a calculation.

You don’t have to feel torn between emotions and numbers. It’s possible to get a divorce settlement that honors both. Here’s how that plays out in five common divorce decisions.

In this article

- Divorce decisions aren’t just financial. They’re a mix of math, emotion, and long-term life design, and all three matter.

- The goal isn’t to “win” every category, but to make smart tradeoffs that protect both your financial future and your emotional bandwidth.

- The best settlements often come from honoring both stability and flexibility, so you can move forward without resentment or regret.

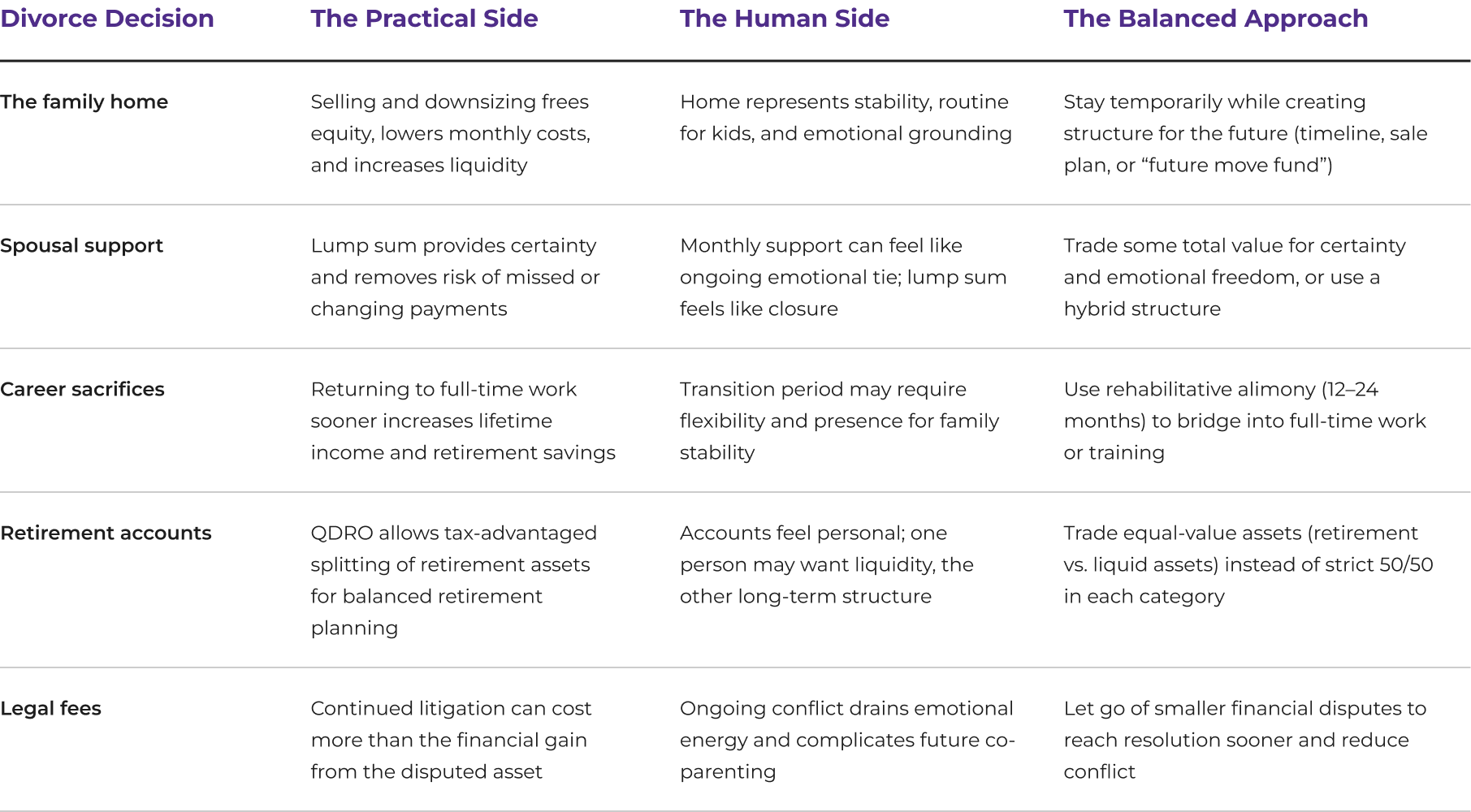

Keeping the home: balancing stability and financial flexibility

The practical side: Selling the home, splitting the equity, and downsizing into something more affordable is usually the most financially efficient move. It reduces overhead fast, helps unlock trapped equity, and gives you more flexibility and breathing room in your monthly budget. In plain terms: it turns a high-cost asset into usable cash and lower ongoing stress.

The human side: Keeping the home is often about stability. It’s routine for your kids, it’s your sense of community, and it’s the place where life feels anchored instead of in motion. That matters.

The balanced approach: You don’t have to choose between financial security and emotional stability today. A middle path could look like staying in the home for a defined timeline while putting structure around the future.

For example: You stay in the home until your youngest graduates but set a pre-agreed sale date, a clear equity buyout plan, or a refinance strategy that protects long-term retirement goals.

You could also structure it as a financial runway plan, where you stay in your home while actively redirecting any savings gains, bonus income, or equity growth toward a dedicated “future move fund.” That way, staying isn’t passive. It’s intentional, time-bound, and working toward your eventual transition.

Spousal support: choosing between a lump sum or ongoing monthly payments

The practical side: A lump sum means financial certainty upfront, removing the risk of missed, reduced, or inconsistent payments down the line if income changes or circumstances shift.

The human side: Monthly payments can feel like an ongoing thread to the past, while a clean settlement can create a stronger sense of closure and personal independence. A lump sum, on the other hand, can feel like a clean line in the sand. It’s not just about money so much as it’s about closing a chapter so your financial life feels like it belongs entirely to you again.

The balanced approach: A slightly smaller lump sum can still be a smart move if it buys you something the spreadsheet doesn’t fully capture: certainty, autonomy, and emotional closure. You’re essentially trading a bit of long-term upside for immediate control and a clean break. For some people, that trade is worth it.

For example: You negotiate a lump sum at 85–90% of the estimated total alimony, giving up a bit of long-term value in exchange for immediate control and certainty. You can then invest or allocate that lump sum intentionally, and you get rid of the ongoing uncertainty of monthly payments, enforcement, or future income changes.

Another option could be a hybrid approach where you get a partial lump sum upfront for stability and transition needs, plus a shorter, time-limited monthly payment schedule. This provides money you can use right away for immediate expenses and early adjustment costs, while also setting a clear end date for the financial arrangement.

Career sacrifices: balancing immediate flexibility and long-term earning power

The practical side: Returning to full-time work sooner increases long-term income, retirement contributions, and financial independence.

The human side: After a major transition, it’s completely normal to need more flexibility and presence at home while things settle and new routines take shape.

The practical approach: You use rehabilitative alimony, a form of temporary spousal support that helps someone build financial independence after divorce. It’s for a defined period of time, say 12-24 months. That time gives you breathing room so you can work part-time, retrain, or stabilize family life, then transition back into full-time work when things feel more grounded.

For example: You could use about 18 months of support to ease back into work at a pace that fits your family right now, especially while your kids are adjusting too. You rebuild routines at home, re-enter the workforce gradually, and increase your hours over time so the move back to full-time feels more steady and sustainable.

You could also use around 24 months of support to focus on completing a certification or degree. That might mean scaling back work temporarily while you build new skills, but it sets you up to step into a stronger earning position (and potentially a higher-paying role) right as the support period naturally comes to an end.

Retirement accounts: splitting vs. trading assets for long-term security and flexibility

The practical side: Splitting retirement accounts (like 401(k)s and IRAs) using a Qualified Domestic Relations Order (QDRO) can create a more balanced, diversified foundation for both parties’ long-term retirement security.

The human side: Retirement accounts often feel personal. One person may feel deeply connected to the account they built or managed, while the other may need more immediate, accessible cash to rebuild and move forward.

The balanced approach: Instead of dividing every account evenly, you can trade assets of equal value. For example, one person keeps more of the retirement account, while the other receives a larger share of more liquid assets like a brokerage account or cash-equivalent funds. This way, one person holds on to long-term retirement structure, while the other gains the flexibility and access they need to start fresh.

For example: You give up part of your claim to a 401(k) balance in exchange for a taxable brokerage account with similar value. They keep the retirement account intact and uninterrupted, while you gain access to funds you can use now for housing, transition costs, or rebuilding stability.

This might also look like trading your portion of an IRA for a larger share of a home equity payout or other cash. Instead of waiting decades to be able to use retirement funds, you get cash today that helps you establish independence, while your ex retains the tax-advantaged retirement account they’re already familiar with managing.

Legal fees: balancing cost, conflict, and resolution

The practical side: Sometimes continuing to fight legally can cost more than it’s worth. For example, spending an extra $20,000 in legal fees to get a $30,000 asset might leave you with only a small net gain once everything is said and done.

The human side: The constant back-and-forth with lawyers can wear you down. The stress and delays can be exhausting.

The balanced approach: In some cases, letting go of smaller financial points can be the smartest move. It helps you reach resolution sooner, protects your emotional bandwidth, and gets you to a place where life can move forward again.

For example: You realize that continuing to fight over a relatively small asset would cost nearly as much in legal fees as the asset is worth. Instead of dragging things out, you agree to a slightly less favorable split on paper, but you get to close the case, stop the ongoing conflict, and start the next chapters.

In review

Here’s a side-by-side comparison summarizing what we’ve just reviewed:

There’s no “right” way to divorce

The family home. Your children’s education. Security in retirement. Everyone’s needs are different and a successful divorce settlement should reflect that. CURO Wealth Management advisors can help you create an agreement to best support you in the next phase.

CURO Wealth Management does not provide legal or tax advice. You should consult a legal or tax professional regarding your individual situation.