Should I Wait to Start My Social Security Benefits?

Deciding when to begin taking your social security retirement benefits can be difficult because there are many factors to consider. Even if you plan to keep working, social security benefits are available to most workers as early as age 62, but you can delay collecting until age 70 or choose any age in between.

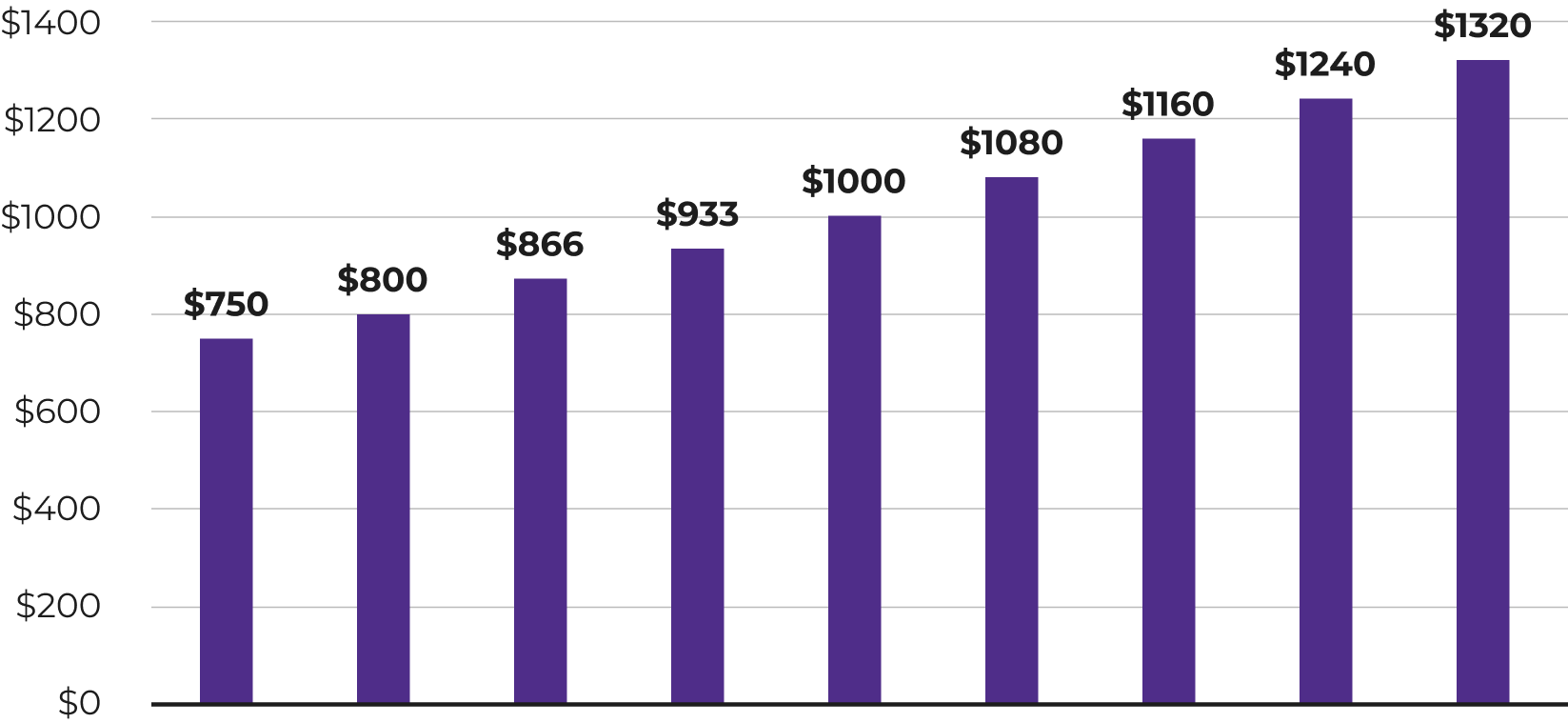

The first step in making your decision is to determine your full retirement age (FRA)—the age at which you can collect your full benefits. For workers born between 1943 and 1954, the FRA is 66; for those born later, the FRA gradually increases by two months to age 67. Claiming benefits prior to your FRA can reduce your monthly payment by as much as 30 percent—but you will collect benefits for a longer period. If you postpone claiming benefits beyond your FRA, your social security payment will increase by a certain percentage, depending on your year of birth, until you reach age 70.

It’s important to consider your options carefully. The decision to claim benefits early may result in a lower standard of living for the rest of your life. And claiming later can mean more financial security for your surviving spouse.

The benefit reduction incurred by claiming early is permanent. If you elect to start receiving benefits early, your benefits will still be increased annually by cost-of-living allowances. But despite social security’s annual inflation adjustment, your payments may never equal the benefit you would have received by waiting until your FRA.

How Benefits Differ Based on Starting Age

Questions to Ask Yourself

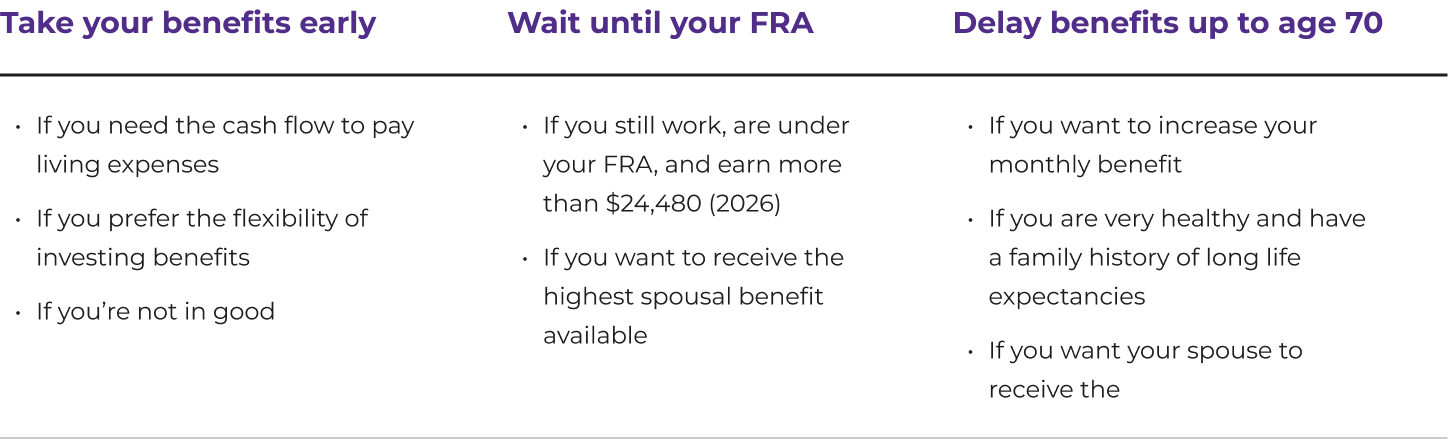

From a purely mathematical point of view, many people are better off waiting to start collecting social security benefits, but there are questions you need to ask yourself.

Do you need the cash?

If you need help paying for basic living expenses, you probably should elect to begin receiving benefits as soon as possible.

How is your health? In any case, it is important to consider your health and your family's pattern of longevity. The longer you live, the more you benefit from delaying. If your health and family history predict a long life, you may be better off delaying your benefits until FRA or later. If you don’t expect to attain a normal life expectancy and you are single, consider taking benefits early. But if you are married, be aware that doing so will reduce your spouse’s survivor benefit.

Will you continue to work?

If your working wages are greater than $24,480 in 2026 and you selected early benefits, your (and your dependents’) social security benefits will be reduced by $1 for every $2 you earn. If you earn more than $65,160 in the year you reach your FRA, your benefits will be reduced by $1 for every $3 you earn. After that point, working has no effect on the amount of your benefit, though it may affect whether your benefits are taxed.

Although your benefits will be reduced if your earned income exceeds the threshold, this is a temporary reduction. The SSA will recalculate your benefits at your FRA and credit any months when your earnings from work completely offset your monthly benefit. Further, since your benefit includes your highest 35 years of indexed earnings, wages you earn today may replace lower-earning years in the benefit calculation, which could result in higher benefits.

Are you in a high tax bracket?

Because social security benefits may be taxed, those in the highest tax brackets and with other sources of income may benefit from delaying social security, thus deferring taxes.

Normally, if both you and your spouse are collecting a benefit, the SSA will pay you the higher of your own social security retirement benefit or 50 percent of your spouse’s FRA benefit. If you were born in 1953 or earlier and delayed benefits until your FRA, however, you could have filed a restricted application. For those born after 1953, however, this is no longer an option.

In order to maximize survivor benefits for the family, one strategy would be for the lower-earning spouse to take reduced benefits after age 62 and for the higher-earning spouse to wait to take a benefit at their own FRA. or later, up to age 70 to accrue delayed retirement credits. If you delay collecting your benefit until after your FRA, your benefit increases by 8 percent per year until age 70.

Are you a surviving spouse?

As a widow or widower at FRA, you are generally eligible for what your spouse’s benefits would have been if they were living. Reduced survivor benefits are available at age 60. Taking a reduced survivor benefit does not affect the benefit based on your own earning history. Thus, you can apply for a survivor benefit and switch to your unreduced retirement benefit at your FRA or later. Conversely at age 62, you can apply for you own reduced retirement benefit first and switch to the survivor benefit at FRA. This decision should be based on your personal situation.

Will you spend or save your social security benefits?

You may be able to earn more on your reinvested payments than you lose by taking a reduced benefit. A tax professional can calculate the after-tax, break-even interest rate that would be necessary for this strategy to make sense. Before you can decide when to take retirement benefits, it’s necessary to check with the SSA to find out which benefits you’re entitled to claim. Verify your earnings history with the SSA’s records and correct any errors. Based on the social security benefit statement and your recent tax records, a tax preparer or financial advisor can run financial models to help you make your decision.

This material has been provided for general informational purposes only and does not constitute either tax or legal advice. Although we go to great lengths to make sure our information is accurate and useful, we recommend you consult a tax preparer, professional tax advisor, or lawyer.